Weekly Market Performance — August 23, 2024

- J. J. Wenrich CFP®

- Aug 23, 2024

- 8 min read

Markets Blog

David Matzko, LPL Research

Weekly Market Performance for the week of August 19, 2024. Focus shifted to the “cowboy state” as the annual Jackson Hole Economic Symposium for U.S. monetary policy makers took place in Wyoming, highlighted by Federal Reserve (Fed) Chair Jerome Powell’s speech on Friday. Stocks sealed solid weekly gains after Powell’s dovish remarks signaled rate cuts are likely on the horizon if economic and labor market data trends continue. Treasury yields came under pressure over the last five days, dipping on reinforced rate cut expectations and Wednesday’s nonfarm payrolls revision. The dollar slipped in reaction to Fed remarks, while oil prices were battered intra-week.

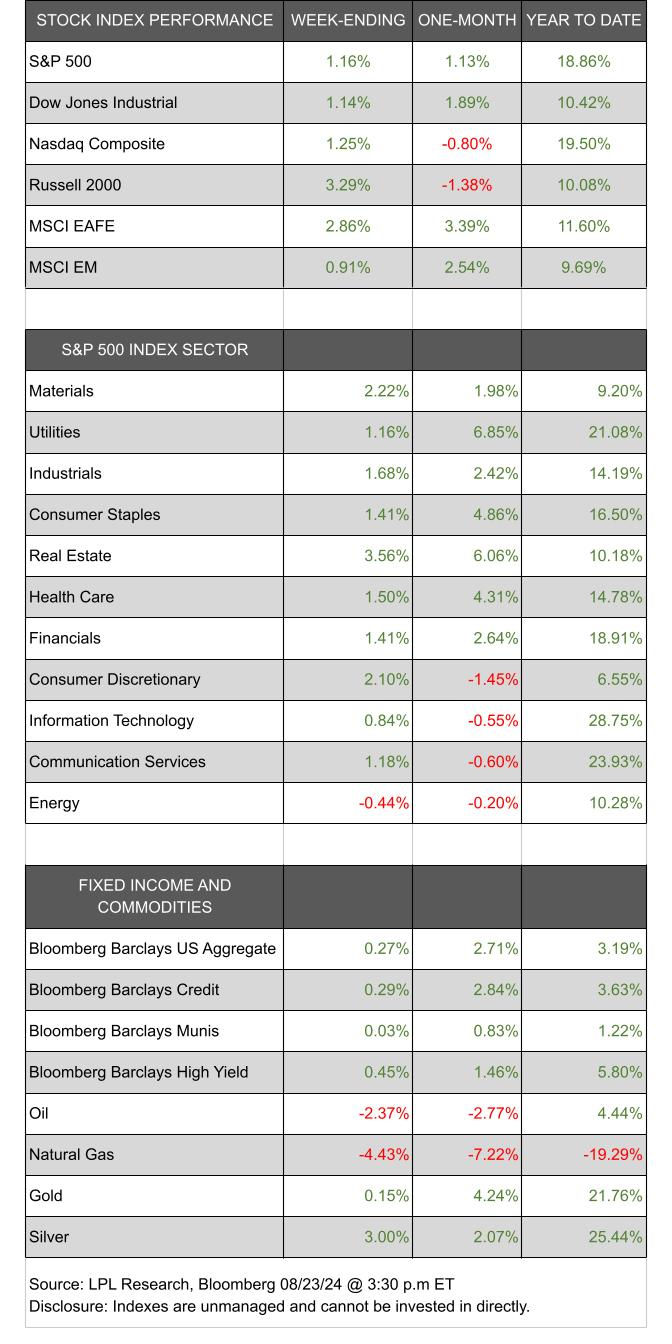

Index Performance

U.S. and International Equities

Markets: Markets took a quick breather from the recent flurries of economic data, and the relatively quiet news flow turned all attention to central bank officials and rate cut expectations. In somewhat muted trading, major indexes continued to advance following a bumpy start to the month of August, as the S&P 500 added 1.1% on the week. The Nasdaq Composite also climbed 1.1% over the last five sessions, while the Dow Jones Industrial Average closed 1% higher.

Rate cut expectations and Federal Reserve (Fed) remarks have remained prevalent throughout 2024, and the annual Jackson Hole Economic Symposium is typically a focal point of headlines. However, with the Fed approaching an inflection point at the September meeting, Fed Chair Jerome Powell's speech on Friday took the spotlight with added importance. Investors were looking for signals around upcoming rate cuts, and Fed Chair Powell appeared dovish in the Fed’s analysis on the state of the economy, stating that the time has come for policy changes. With Jackson Hole in focus and a relatively light macro calendar, trading volume was thin most of the week. Stocks slid Thursday on a slight fall in the flash composite Purchasing Managers' Index (PMI) for August, while existing home sales sluggishly increased as buyers took advantage of increased opportunities. Meanwhile, an unexpectedly large preliminary revision to nonfarm payrolls (for the 12 months ending in March) surprised investors, as the labor market appeared weaker than originally reported. On the earnings front, retail names were in focus, including an earnings and sales beat from Target (TGT) while home improvement retailer Lowe's (LOW) earnings beat was offset by slashed guidance.

Central banks were also in focus in European markets, as the European Central Bank (ECB) also approaches their September policy meeting. The STOXX 600 index of European markets closed 1.31 higher on bolstered rate cut hopes on comments from ECB policy makers around economic growth risks and openness to further rate cuts. Additionally, Eurozone PMI propelled markets on Thursday after receiving a boost from French services following the Olympic Games in Paris. Outside of economic news, the European Union (EU) announced a revision of previously announced tariffs on Tesla vehicles from China, reducing potential tariffs from 20% to 9%. Corporate headlines took a step back from the spotlight, however, shares of Nestle SA slipped after the unexpected replacement of their CEO.

Asian markets ended broadly higher, driven by PMI and CPI data across the region. Japan ended higher following a slight CPI increase, although in-line with estimates, and a slower increase in manufacturing PMI due to increasing output. China fell in relatively quiet trading, after the People's Bank of China (PBOC) held one- and five-year loan prime rates unchanged. Plus, China responded to updated EU tariffs with an anti-subsidy investigation into daily imports from Europe. Hong Kong ended higher despite oil and gas stocks struggling intra-week, while South Korea and Taiwan closed mostly lower. India experienced solid gains and Australia inched higher on an extended winning streak and PMI shrinking at a slower pace.

Fixed Income: The Bloomberg Aggregate Bond Index traded higher this week, as the bond market continued to adjust to fluctuating rate cut odds, this time focused on Fed Chair Powell’s highly anticipated speech in Jackson Hole. The 10-year Treasury yield ended eight basis points lower, while the monetary policy-sensitive two-year yield finished nearly 15 basis points lower.

Over recent weeks, markets have priced in aggressive Fed rate cuts and will likely continue to do so after Powell’s remarks on Friday signaled the Fed’s readiness to cut rates in the future. Yields fell following Powell’s speech, after briefly recovering from recent lows midweek. Yields came under pressure most of the week, hovering near one-year lows as the nonfarm payrolls revision and an increase in jobless claim applications backed rate cut expectations. Market liquidity conditions have largely rebounded amid the recent decline in volatility, as macro data over the last few weeks assuaged fears surrounding an economic slowdown. Additionally, Treasury yields and corporate spreads have largely retraced their post-payrolls move, also finding support from the relative strength of the economic data and normalization in risk sentiment. Markets will be focused on initial jobless claims next week, as it will overlap with the employment survey reference week in the wake of Fed Chair Powell’s citing of increased downside risks to the labor market.

Commodities and Currencies: The Bloomberg Commodities Index closed 0.87% higher this week. West Texas Intermediate (WTI) crude ended 2.25% lower, although bouncing back from mid-week lows after a sell-off sparked by the U.S. jobs data revision battered oil prices. Focus also remained on weak demand from China, the number one importer of oil, as well as ceasefire talks to end the war in Gaza which reduced concerns the conflict would impact oil supplies. The U.S. dollar index traded lower on dovish Fed meeting minutes and sank further after Fed Chair Powell’s signal that rate cuts were on the horizon. The Japanese yen moved higher following hawkish comments from Bank of Japan (BOJ) Governor Ueda signaling policymakers are open to further rate hikes. Additionally, carry trades that blew up markets just a few weeks ago appear to have been flushed out. Gold jumped on Friday to end the week relatively flat, while silver added over 2% and copper pared gains to end flat.

Economic Weekly Roundup

Fed Chair Powell Noted “An Evolving Landscape”. Chairman Powell focused on the fragilities of the labor market and is preparing markets for the new phase for policy. “The time has come for policy to adjust.” Powell specifically highlighted the labor market 27 times in his speech Friday morning, indicating the current focus for the Federal Open Market Committee (FOMC). He surprisingly talked about the “transitory hypothesis” and tacitly defended the argument for that perspective. A soft landing looks achievable, barring any shocks. Disinflation while preserving labor market strength is only possible with anchored inflation expectations, so an independent and credible central bank is key.

One of the best concepts in today’s speech for investors to understand is the current data show an evolving macro landscape. The jury is still out on if the Fed can successfully manage the risks to both sides of their dual mandate. However, Chairman Powell could not be clearer — “the time has come for policy to adjust.”

Final Nonfarm Payroll Revisions Could be More Than Normal. Wednesday’s preliminary estimate indicated a downward revision by roughly 800,000 in the 12 months through March. For perspective, last year’s preliminary estimate was 306,000 fewer payroll jobs than originally reported. Average annual revisions over the past decade were +/- 0.1% of total employment. For this current round, the revisions indicate an adjustment of -0.5%. The final benchmark revision will be published in February next year. Industries with the largest negative revisions were professional services and hospitality sectors. In contrast, transportation and warehousing industries are expected to be revised higher. It’s not surprising that the Leisure and Hospitality sector is the most volatile.

The labor market appears weaker than originally reported. A deteriorating labor market will allow the Fed to highlight both sides of the dual mandate and investors should expect the Fed to prepare markets for a cut at the September meeting. A weaker-than-expected job market could pave the way for the Fed to cut by a half-percentage point in September.

The Week Ahead

The following economic data is slated for the week ahead:

Monday: Durable Goods Orders (July preliminary), Durable Goods Orders ex Transportation (July preliminary), Capital Goods Orders Nondefense ex Aircraft (July preliminary), Capital Goods Shipments Nondefense ex Aircraft (July preliminary), Dallas Fed Manufacturing Activity (August)

Tuesday: FHFA House Price Index (June), House Price Purchase Index (Q2), S&P Core Logic Case-Shiller 20-City Home Price Index (June), S&P Core Logic Case-Shiller U.S. Home Price Index (June), Conference Board Consumer Confidence, Situation, and Expectations (August), Richmond Fed Manufacturing Index (August), Richmond Fed Business Conditions (August), Dallas Fed Services Activity (August)

Wednesday: MBA Mortgage Applications (August 23)

Thursday: GDP Annualized (Q2), Personal Consumption (Q2), GDP Price Index (Q2), Core PCE Price Index — quarter-over-quarter (Q2), Advance Goods Trade Balance (July), Wholesale Inventories (July preliminary), Retail Inventories (July), Initial Jobless Claims (August 24), Continuing Claims (August 17), Pending Home Sales (July)

Friday: Personal Income (July), Personal Spending (July), Real Personal Spending (July), PCE Price Index (July), Core PCE Price Index – month-over-month and year-over-year (July), MNI Chicago PMI (August), University of Michigan Report (August final)

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax.

Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: 619684

Comments